Family values and traditions are a vital legacy, but financial education provides the tools to help sustain them. Among all the gifts you can leave behind, teaching the concept of compound interest can be one of the most valuable. From a young age, children receive piggy banks, open their first savings accounts, and receive gifts intended for their future. While the primary emphasis is on saving, there is often less focus on the principles that can allow those assets to grow over time.

Simple Interest vs Compound Interest

Most understand simple interest: banks pay a small “thank you” for deposited money – interest is only earned on the principal balance. However, compound interest is calculated not just on the initial investment, but also on all the interest accumulated. In simpler terms: it’s interest earning interest.

The key components of compound interest are:

- Principal: Initial capital.

- Interest Rate: Annual growth rate.

- Time: The duration your money stays invested.

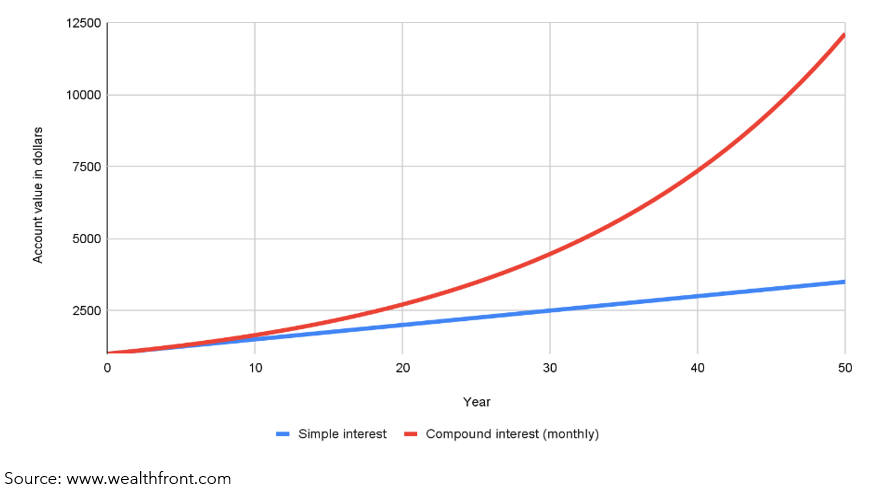

Let’s compare the two types of interest for a $1,000 investment at a 5% interest rate over 50 years1:

- Simple Interest: You earn $50 every year. After 50 years, you have $3,500.

- Compound Interest (monthly): Your interest starts earning its own interest. After 50 years, that same $1,000 is worth $12,119.38.

As the following graph illustrates, an account with compounding interest doesn’t just grow your money, it has the potential to turn modest savings into significant wealth over time. The key concept is time: the longer your capital remains invested, the steeper that growth curve can become.

Time

The real difference between simple interest and compound interest becomes apparent over time.

Consider $10,000 invested over different time periods1:

| Time Period (Years) | Simple Interest 5% | Compound Interest 5% Annually |

| 10 | $15,000 | $16,289 |

| 30 | $25,000 | $43,219 |

| 50 | $35,000 | $114,674 |

This table highlights how compound interest can have a meaningful impact on investments over time. The longer the funds stay invested the larger the difference is noticed between the two types of interest.

One of the significant mistakes our younger generation may make is assuming they don’t have enough money to begin investing or to make a difference. In terms of compounding, their greatest asset isn’t the size of their paycheck, but rather the amount of time on their side.

Starting the Conversation Early

Many effective lessons about compound interest can begin with basic conversations during childhood and adolescence. Here are some examples:

- Open an investment account early – Small contributions to a custodial brokerage account or Roth IRA (if the child has earned income) can demonstrate growth over time.

- Statements – Show children investment statements to see the long-term growth.

- Match contributions – If a child invests $100, offer a match to reinforce saving and investing habits.

- Share your story – When you started investing, what to avoid, and what you wish you knew when you were younger.

Summary

The transfer of financial knowledge across generations can be one of the most meaningful investments a family can make. Teaching younger family members about compound interest may encourage them to invest early, practice patience and think long-term. Families can create habits that may build financial stability for generations.

Start early. Stay consistent. Let time work for you.

1The information in the example and table shown are hypothetical and provided for illustrative purposes only. They assume a constant 5% rate of return and do not reflect the impact of taxes, fees, inflation, or market fluctuations. These examples are not indicative of actual investment results. Actual results will vary.

This content is provided for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Investing involves risk, including the potential loss of principal.